Beyond Just Money Transactions: Redesigning Digital Peer-to-Peer Payments for Social Connections

Overview:

This project investigates the evolving landscape of interpersonal financial transactions through digital peer-to-peer (P2P) payments (i.e., transferring money between two individuals using banking accounts or credit/debit cards through an online or mobile service for everyday activities), which have significantly altered the dynamics of money exchange between known contacts (e.g., family, friends, colleagues, neighbors, acquaintances). Recognizing the sensitive role of money in social relationships, the project aims to understand how digital P2P payments influence these interactions financially and socially. The ultimate goal is to redesign current digital P2P payment systems to prioritize human-centric interactions, cultural sensitivity, and social satisfaction, by deeply exploring the nuanced experiences of users in their personal financial exchanges mediated by the technology.

Roles:

Led the multi-year project; Conceptualized the framing and research questions; Did literature review; Collected and analyzed the data; Translated findings into actionable insights/recommendations; Wrote manuscripts

Publications:

Lingyuan Li, Guo Freeman, & Donghee Yvette Wohn. (2021). The Interplay of Financial Exchanges and Offline Interpersonal Relationships through Digital Peer-to-Peer Payments, Telematics and Informatics, 101671.

Lingyuan Li, Guo Freeman, & Bart Knijnenburg. (2024). Beyond Just Money Transactions: How Digital P2P Payments (Re)shape Existing Offline Interpersonal Relationships. Proc. ACM Hum.-Comput. Interact. 8, CSCW1, Article 24 (April 2024), 36 pages.

Lingyuan Li, Guo Freeman, & Wen Duan. (2024). Exploring Redesigning Digital P2P Payments to Facilitate Social Connections: A Participatory Design Approach. In Extended Abstracts of the CHI Conference on Human Factors in Computing Systems (CHI EA '24), May 11–16, 2024, Honolulu, HI, USA.

Research Questions:

1. How do people perceive and experience both positive and negative impacts of using digital P2P payments on their interpersonal relationships with known contacts?

2. How can future digital P2P payment systems be designed to better support people's social connections with known contacts?

cr: Unsplash

cr: Unsplash

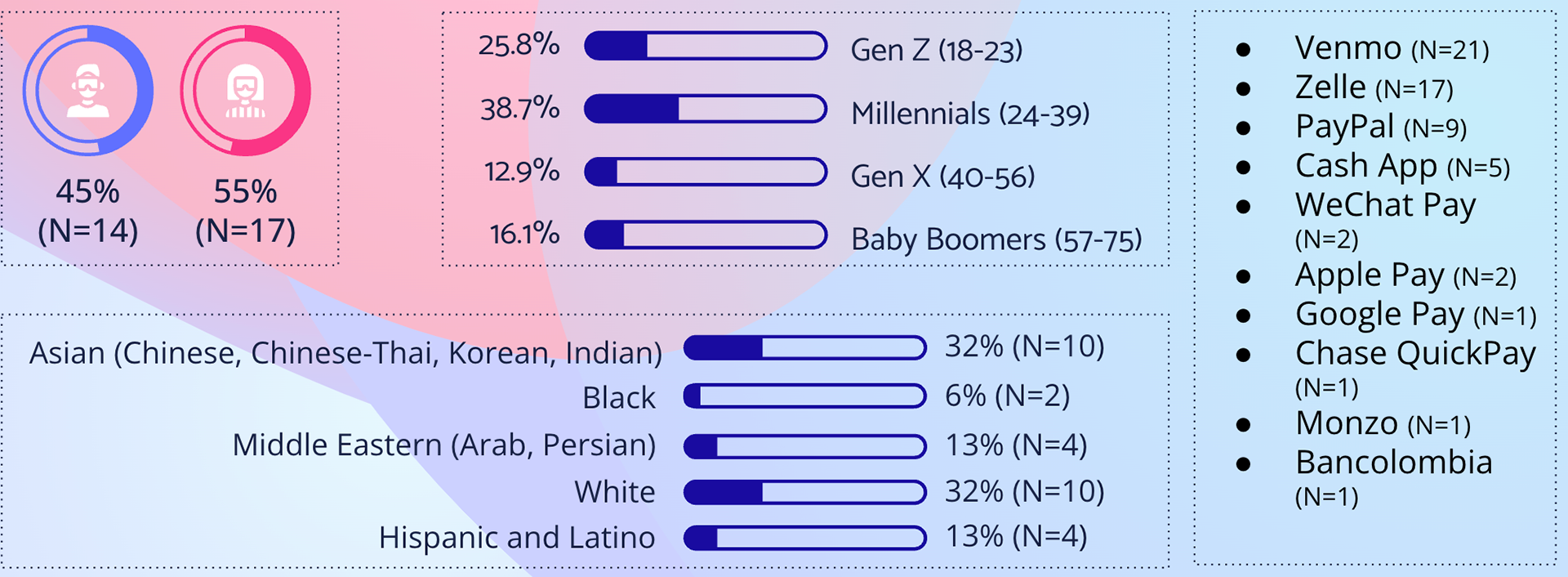

Some popular nonbank provider P2P payment apps: Venmo, CashApp, Apple Pay, Messenger Pay, WeChat Pay, PayPal, Google Pay, Samsung Pay

Some P2P apps supported by financial institutions: Zelle, Bancolombia App, Chase QuickPay, Monzo App

Methods

31 in-depth semi-structured interviews

Qualitative analysis: thematic analysis

Results

Positive immediate social consequences:

① It reduces awkwardness: instant payments, less delayed payments, less personal and more neutral way to communicate finance-related information with known contacts, and easier access to transaction records

② There is a stronger sense of fairness: ensured reimbursement; precise payments

Negative immediate social consequences:

① It increases peer pressure: having to adopt digital payments; having to download specific apps

② There is less emotion in the transaction process: emotions involved in face-to-face personal interaction and communication is eliminated or not needed

Positive lasting impacts:

① It promotes trust: more confident about personal connections; reduce the potential distrust and cognitive load when dealing with money

② It relieves tensions: avoid the mess of rounding up/down; loosen stress on tight finance; get assured from digital-P2P-payment-mediated transactions

Negative last impacts:

① It affects emotional attachment to the sender/recipient: a sense of detachment between known contacts; however, increase emotional attachment for distance relationships and weak social ties

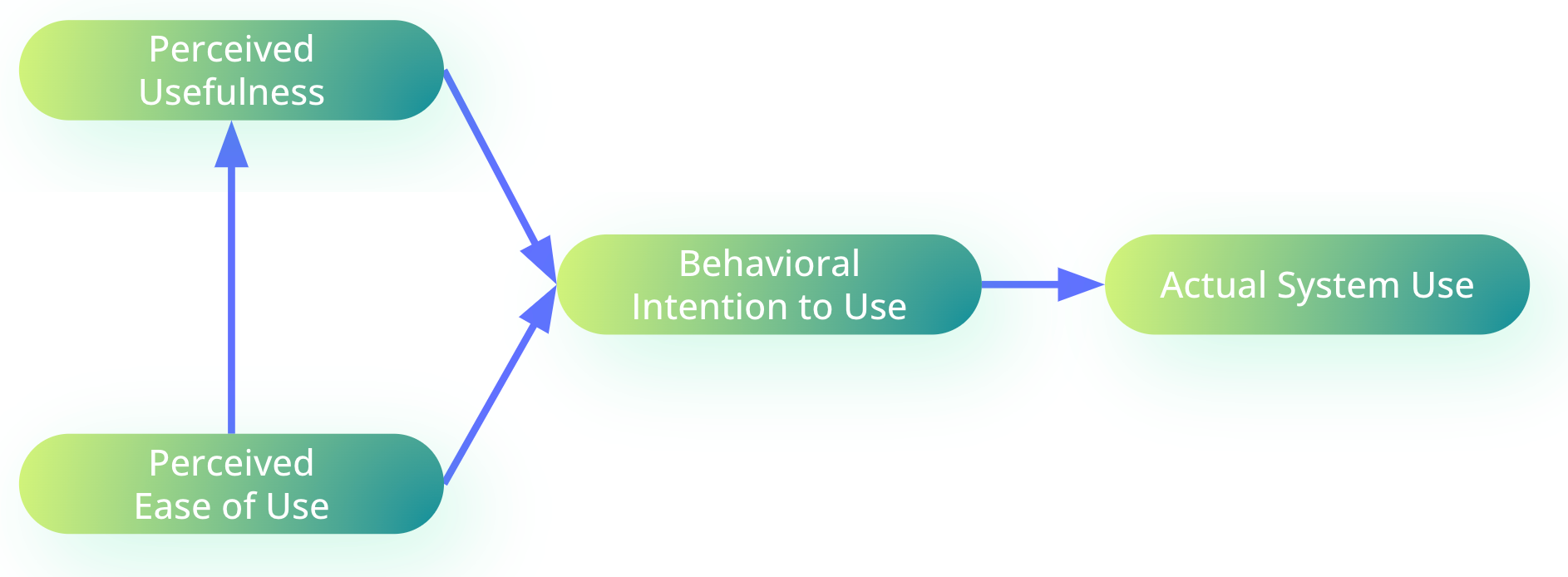

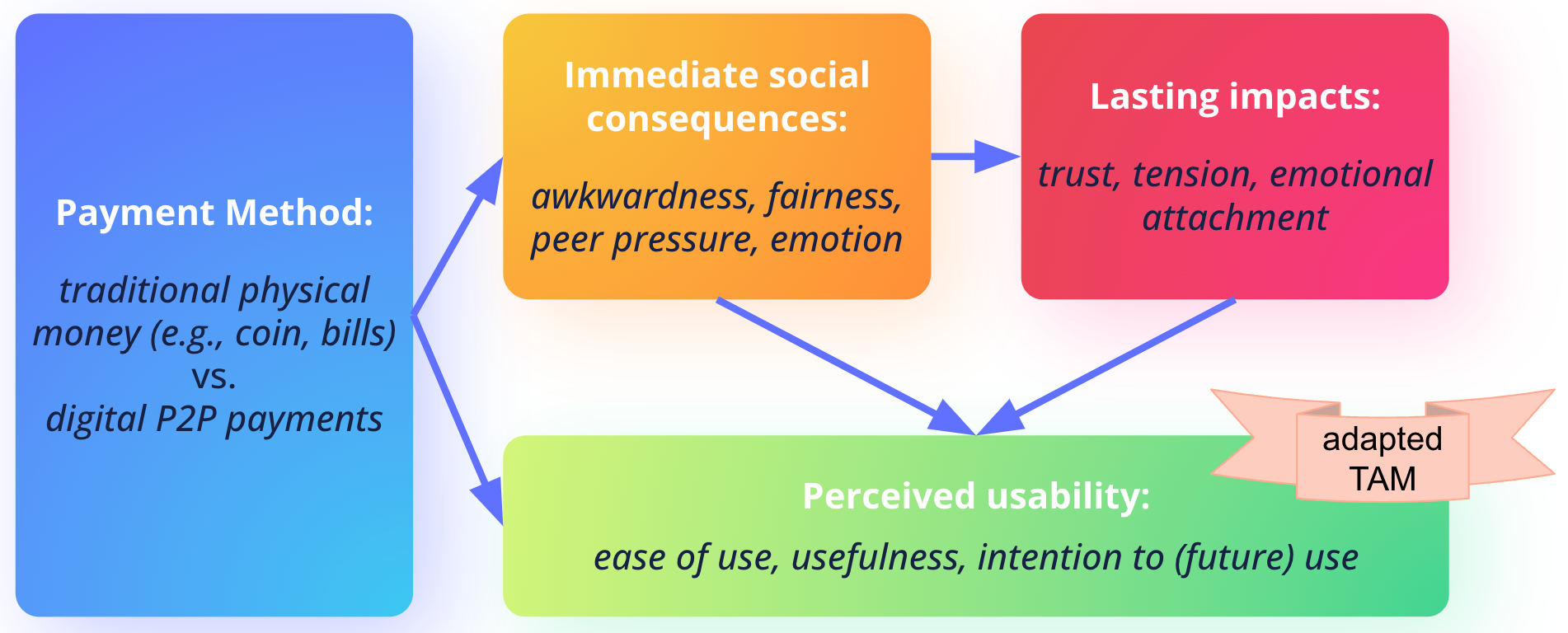

Technology Adoption Model (TAM)

Our Conceptual Model

MethodS

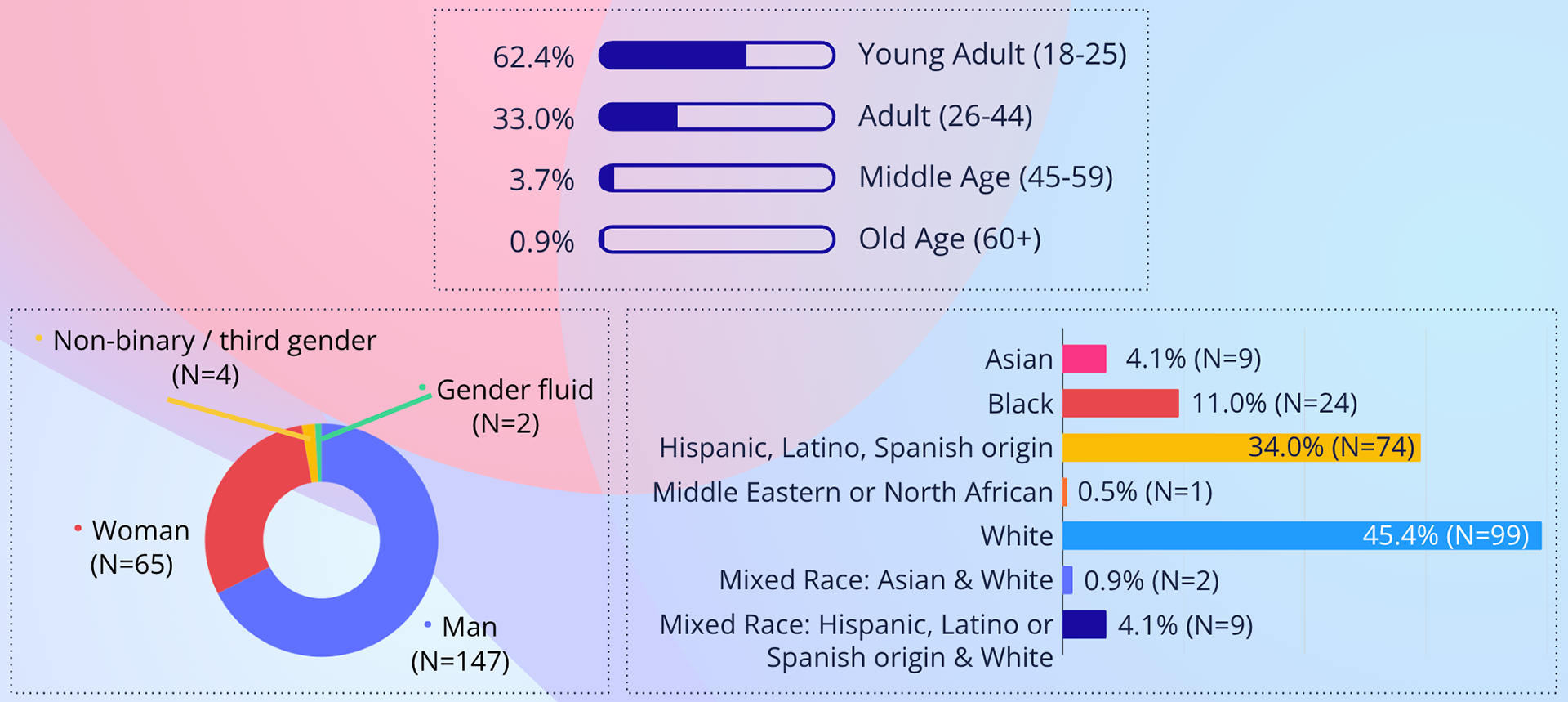

Large-scale anonymous survey via Qualtrics and Prolific

218 valid responses

Quantitative analysis: CFA (remove unqualified factors); T-test; Structural Equation Modeling (SEM)

Results

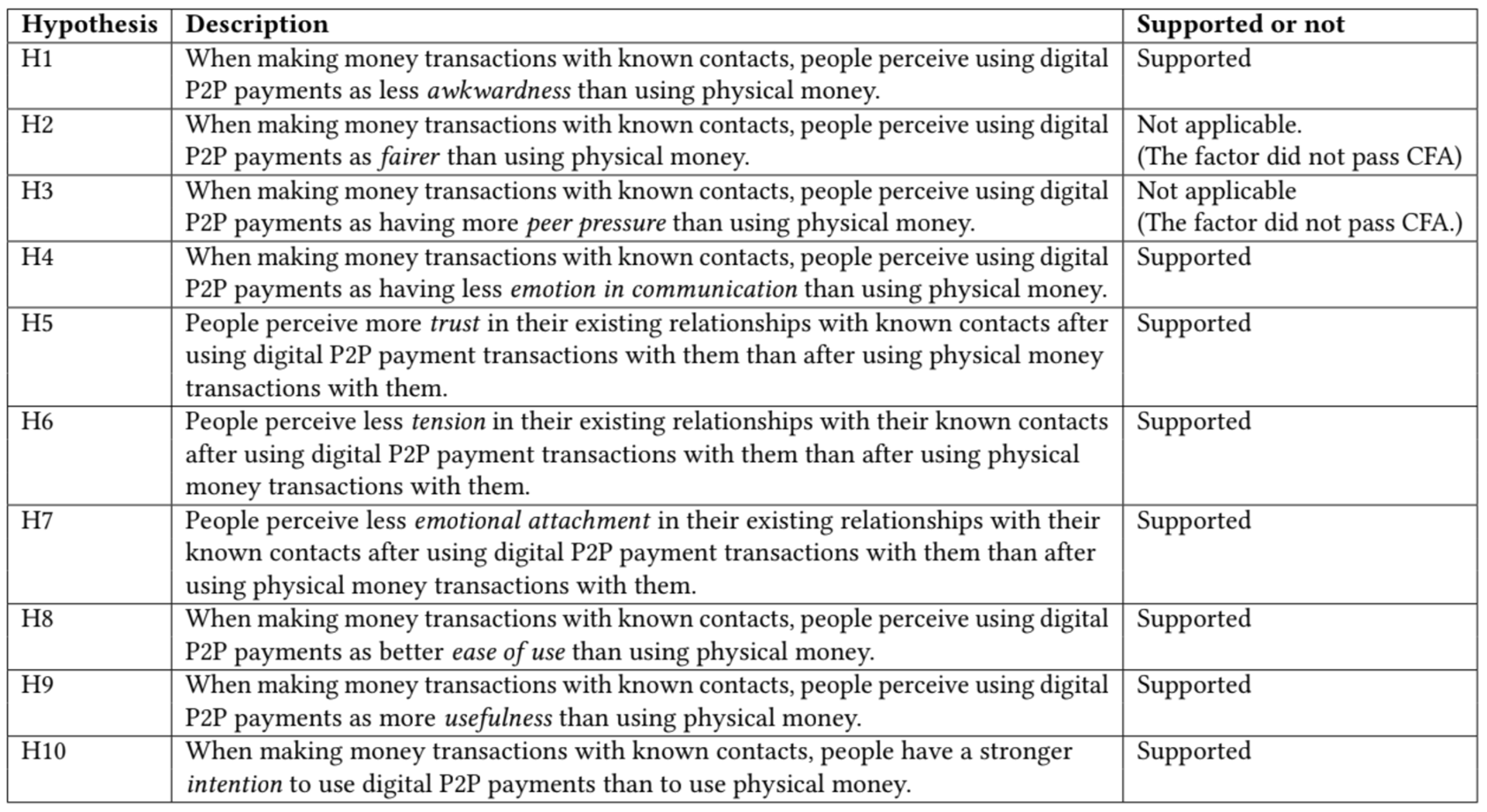

Physical money vs. digital P2P payments:

The differences between them are statistically significant across immediate consequences, lasting impacts and perceived usability. All hypotheses are supported after removing unqualified factors.

Further confirm the results from RQ1 - Phase 2:

Compared to physical money, using digital P2P payments significantly leads to:

① Less awkward and less emotion in communication

② More trust, less tension, and less emotional attachment

③ More ease of use, more useful, and stronger desire to use digital P2P payments for money transactions with known contacts in the future

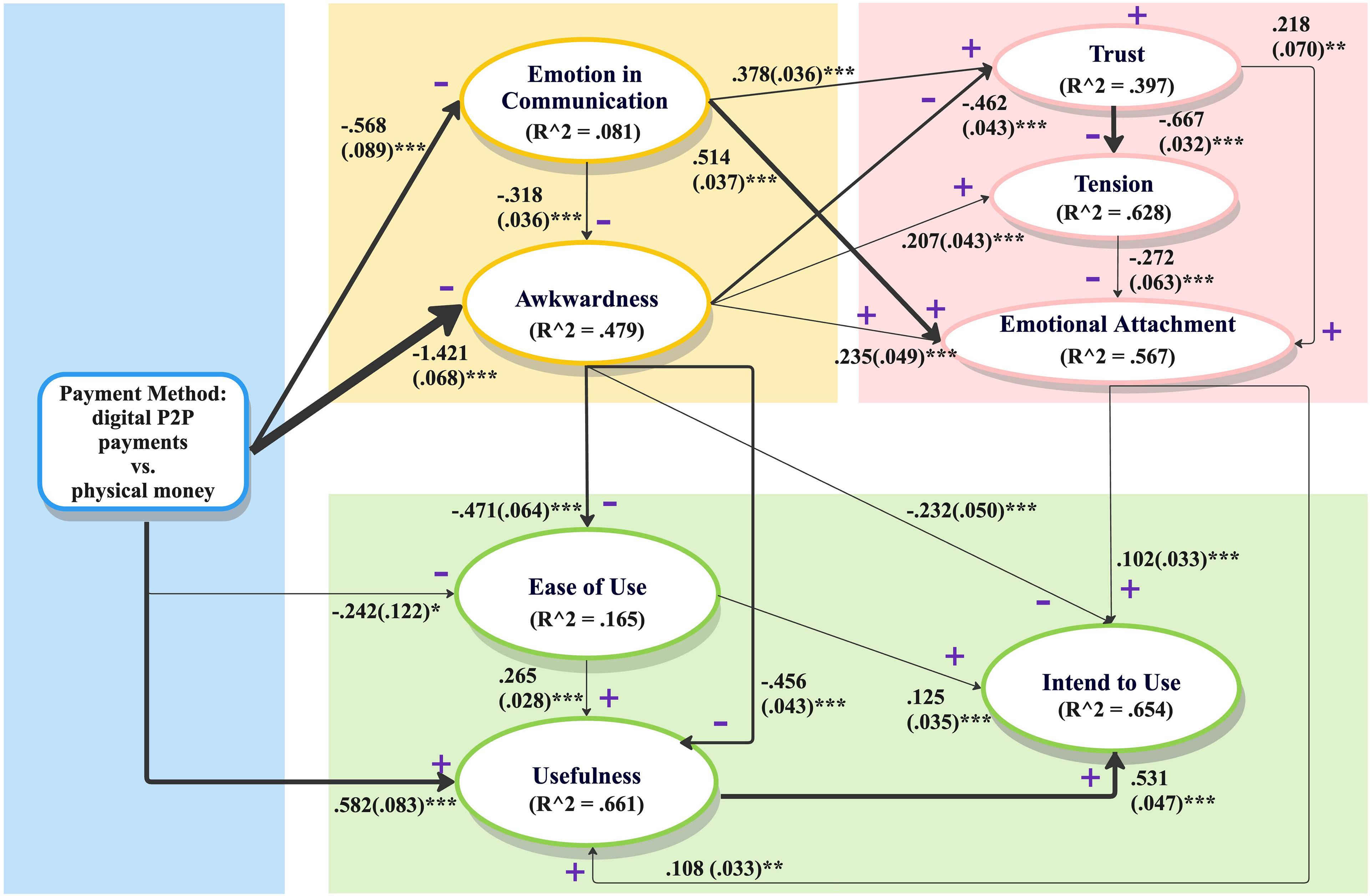

How and why do such differences occur?

① Emotion in communication & awkwardness affect trust;

② Awkwardness & trust affect tension;

③ Emotion in communication, trust, & tension affect emotional attachment;

④ Payment method & awkwardness affect ease of use;

⑤ Payment method, awkwardness, emotional attachment, & ease of use affect usefulness;

⑥ Awkwardness, emotional attachment, & ease of use affect intention to use

What features or functions future digital P2P payment services should have to

1) further strengthen positive immediate social consequences and lasting impacts?

2) mitigate negative social consequences and lasting impacts of using digital P2P payments?

methods

Research through Design coupled with Participatory Design: 2 rounds of workshops

How Might We, Crazy 8’s

Qualitative analysis: thematic analysis

Results

5 participants as co-designers: 3 as man, 2 as woman

White (N=2); Asian (N=3)

Age: 24 - 30 years old (avg: 26.5)

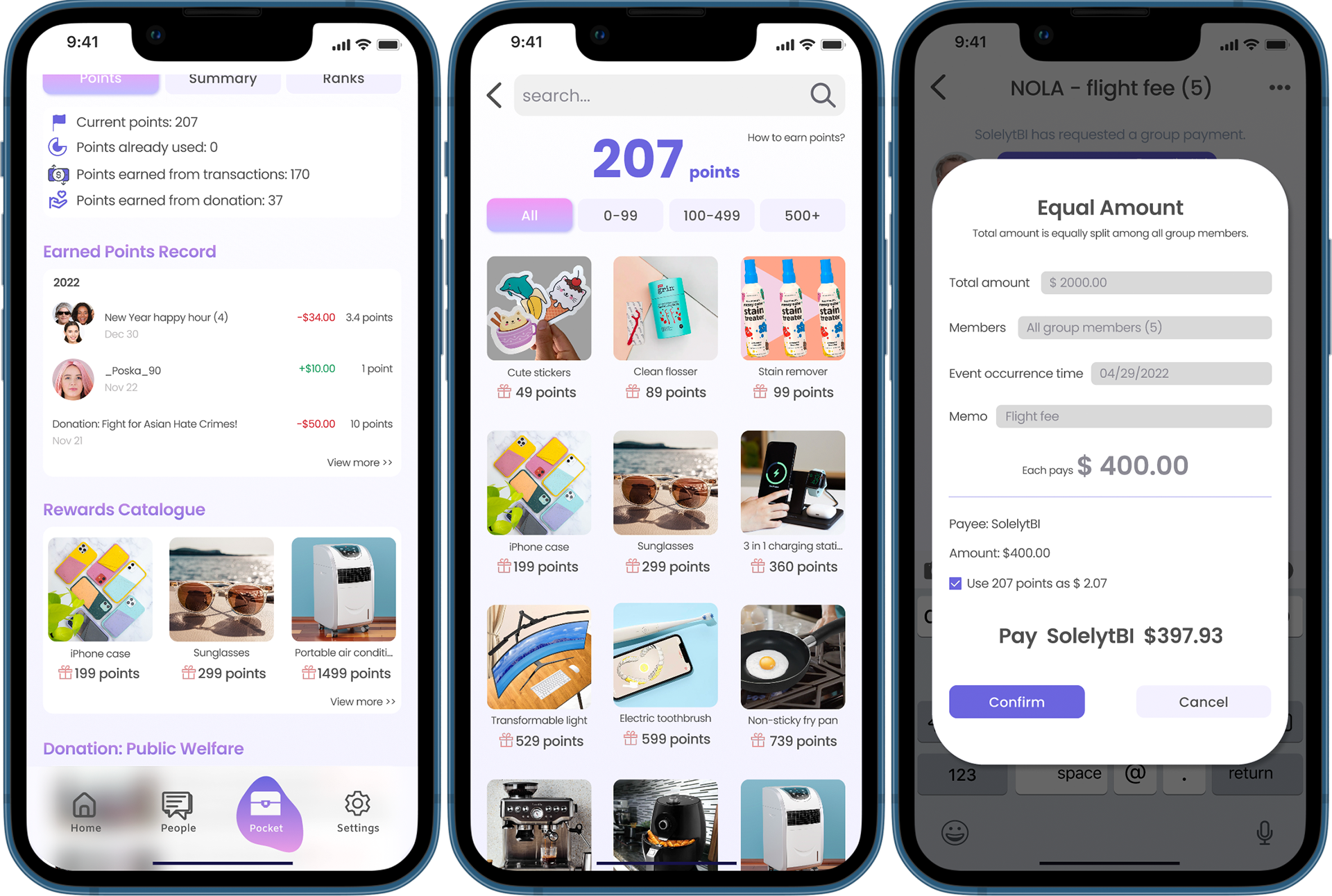

Envision 1: Understanding and Designing for Reducing Awkwardness

E.g., customizable urgency levels for the reminders, sent as official platform messages rather than direct personal prompts, allowing users to tactfully nudge others about repayments without causing embarrassment.

E.g., People can choose which shape they expect the virtual banknotes to look like, making interactions more captivating and informal and diminishing the awkwardness by infusing a sense of fun into the transaction process.

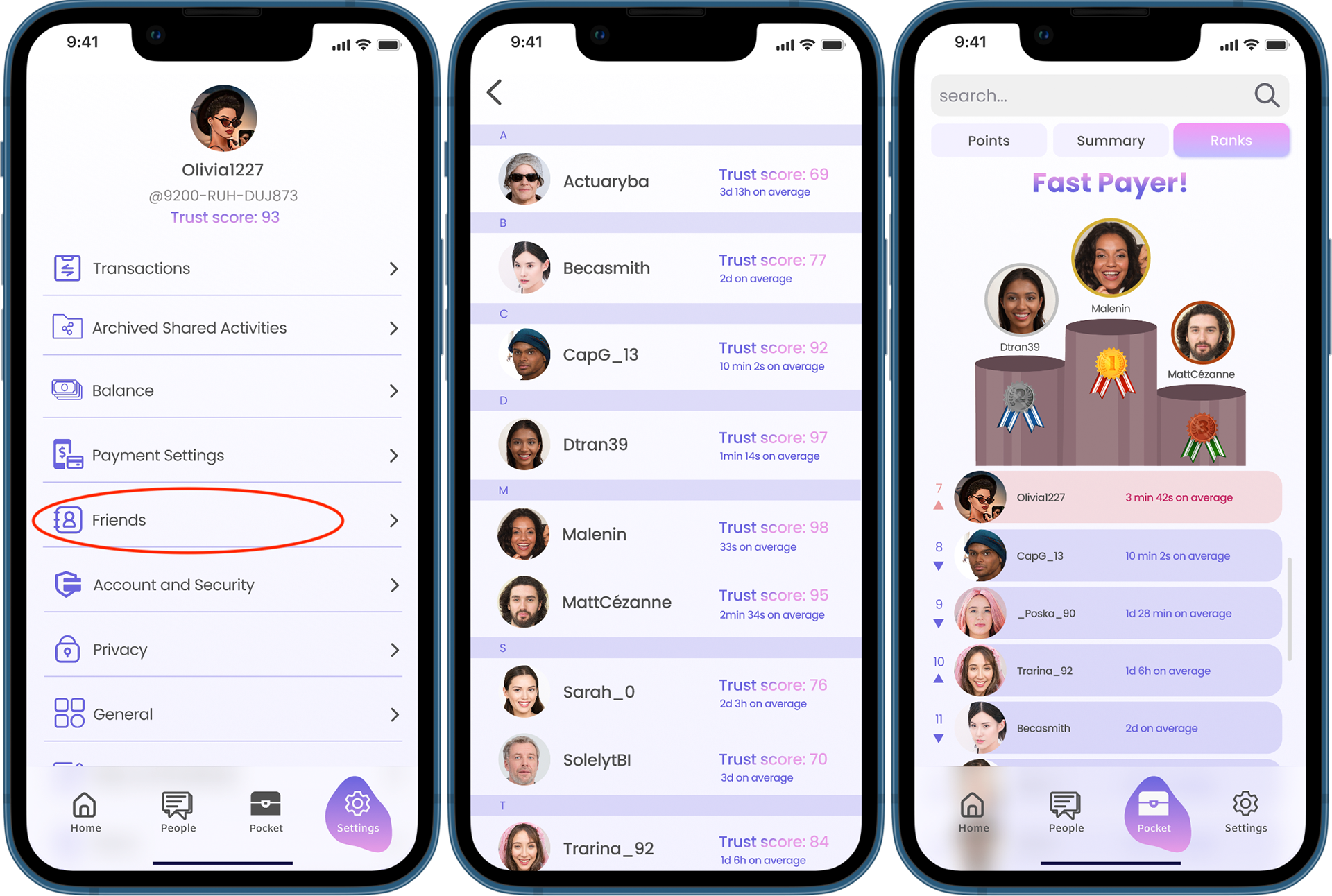

E.g., The app-wide trust ranking highlights users known for their reliability in transactions, motivating users to uphold their financial reputation within their social circles to foster a culture of punctuality and responsibility, reducing awkwardness and potential conflicts.

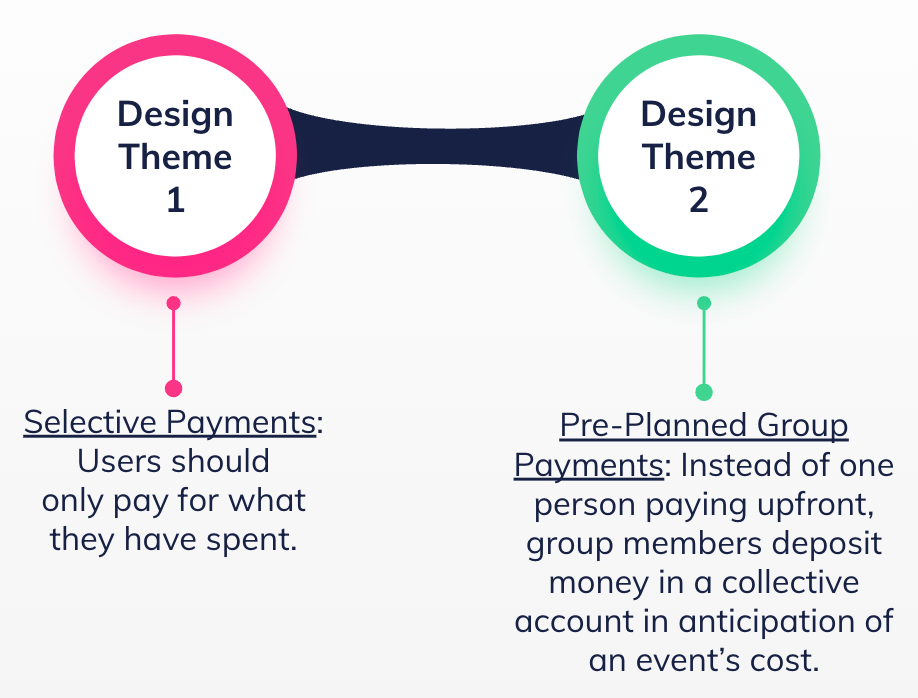

Envision 2: Understanding and Designing for Ensuring Fairness

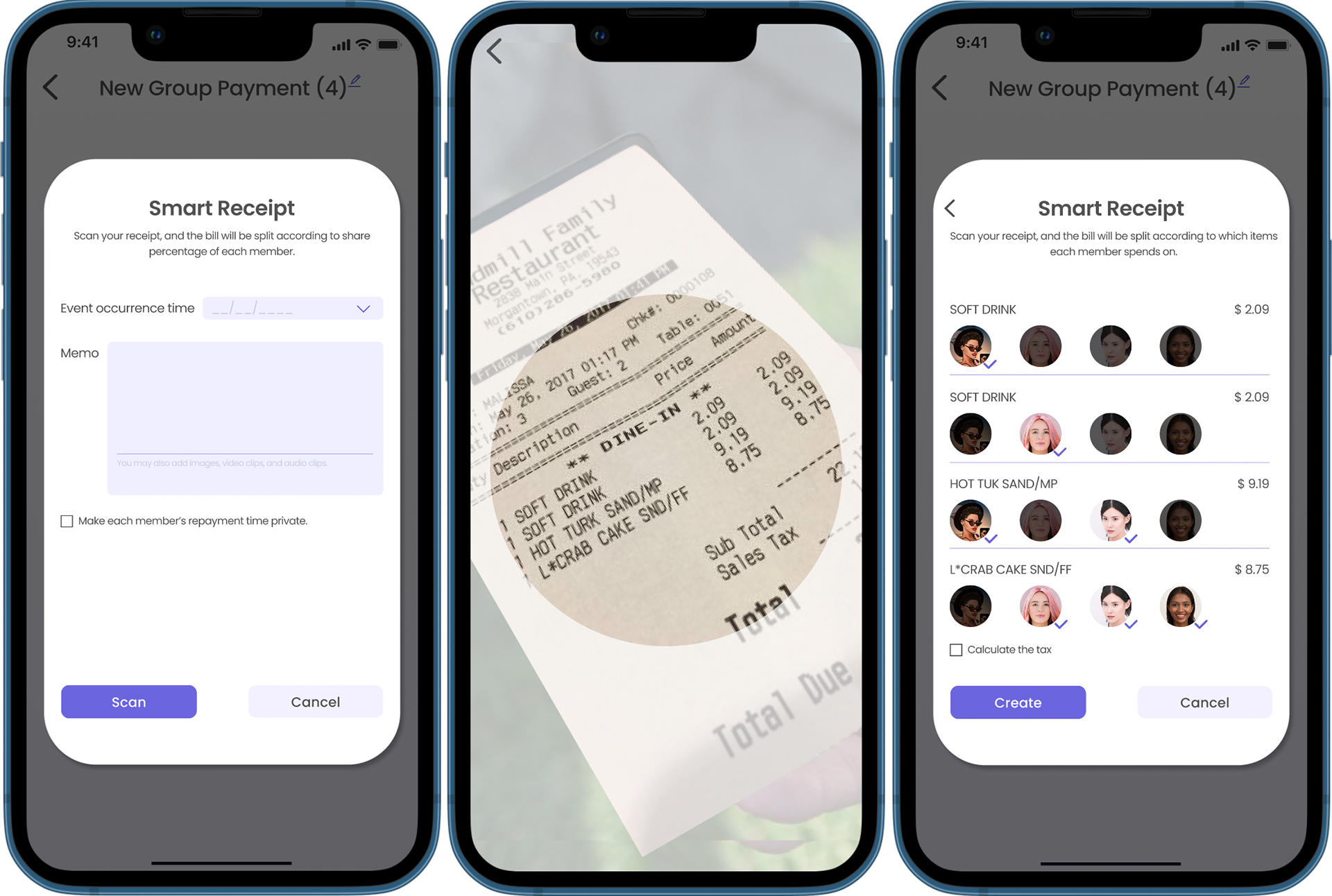

E.g., by scanning a receipt, the system automatically detects listed items, enabling users to select items they need to pay

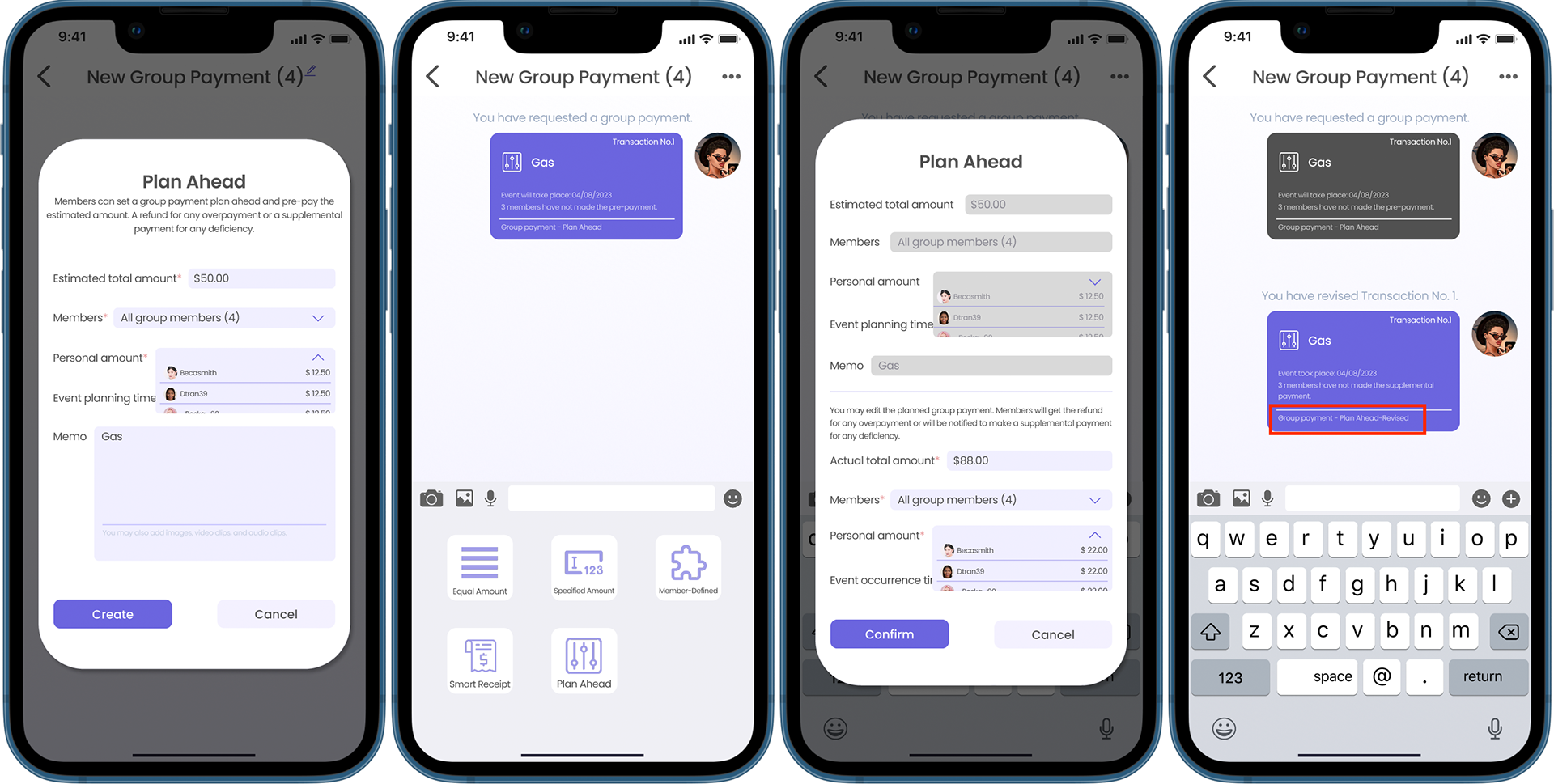

E.g., group members deposit money in a collective account in anticipation of an event's cost. The account can be adjusted post-event to match the actual spending, with members receiving refunds or making additional contributions as necessary.

Envision 3: Reducing Peer Pressure in Digital P2P Payments Adoption

E.g., incentives like earning points from transactions or enabling donations through the app for rewards or to offset transaction costs, thereby shifting perceptions from obligation to personal benefit and interest.

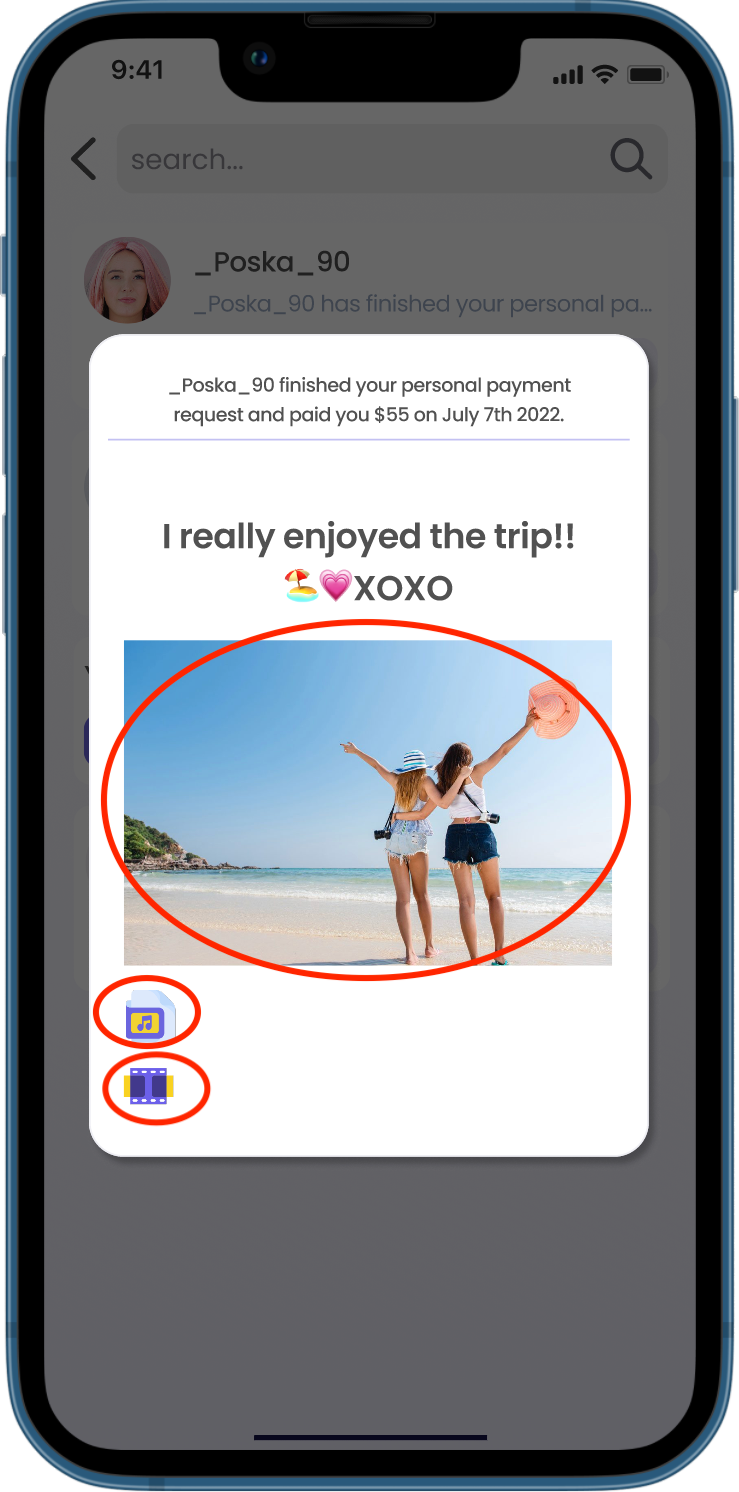

Envision 4: Fostering Emotional Connectivity in Digital P2P Payments

E.g., using various expressive formats in messages, like video, audio, text, or images, for more vivid and explicit communication in digital transactions.

E.g., simulating the act of handing over cash through AR technology